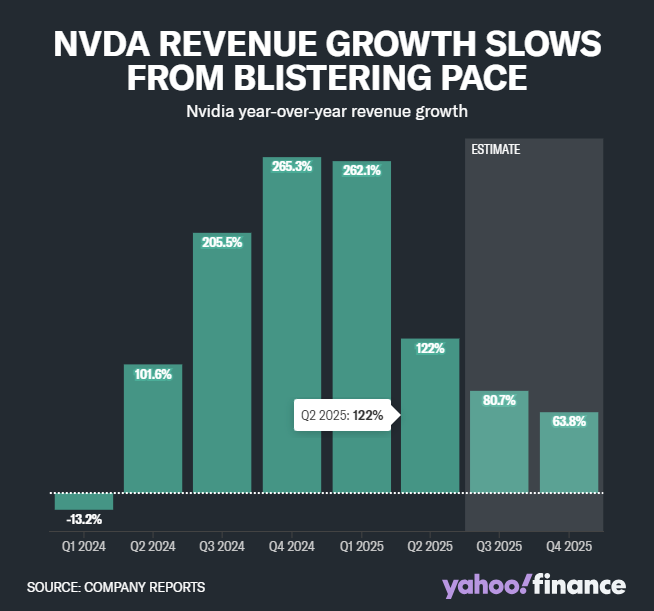

어닝은 여전히 놀랍지만, earning growth가 예전만 못하고 Blackwell에 대해서 자신감있게 말하는것과 달리 현재 루머로 나오고 있는 chiplet을 포기해야 한다는 치명적인 문제까지 해서, 마켓은 썩 좋아하지는 않는 모습. 다행히 NVidia만 떨어지고 다른 반도체 주식들은 선방하고 있음.

샤오미가 어럿 죽여내보내고 있습니다. 오늘 fitbit이 시장에서 14%정도 계속 급락하다가 -12%선에서 마무리했습니다. 핏빗은 한주동안에 26%가까이 급락했습니다. 가장 큰 이유는 샤오미가 발표한 미밴드 펄스때문입니다. Xiaomi Mi Band 1s Pulse. 심박(심장박동) 센서를 내장하고도 가격은 거의 그대로고 배터리 life는 20일이나 된다고 합니다. 전 모델은 연결을 끊고 중간중간 싱크만 하면 2달도 가능하다는 친구를 봤습니다. 보여주는 것이 아무것도 없다지만 정말 대단한 저전력입니다.

영어권 페이지에는 기존 중국모델에서 동양적 이미지의 예쁜 서양모델을 기용했습니다. 페이지도 깔끔하고... 예쁘네요. 샤오미 마케팅이 점점 세련되네요.

벌써 unbox영상이 올라와있는데 상당히 깔끔합니다. $16라는 가격이 믿기지 않습니다. 이거 띠어다가 미국내에서 장사해도 돈 벌겠습니다. (물건을 받을수가 있어야지)

중국에서는 이미 판매중인것으로 나오고요, 전세계 시장에 얼마나 퍼저나갈것은 생산에 달려있겠죠. 샤오미 특성상 이번년내에 중국밖에서 쉽게 구할수는 없을것 같습니다.

가격이 $16정도로 이건 있을수 없는 가격입니다. 핏빗의 경쟁 재품은 Fitbit Charge HR이 이와 비슷한데 핏빗것은 소비자가는 $150로 무려 10배나 비쌉니다.

핏빗은 사실 하드웨어 회사가 아니고 소프트웨어 회사라 좋은 소프트웨어가 무기입니다. 마케팅도 상당히 잘하는 것으로 보입니다. 이 두 부분은 샤오미가 아직 따라오기 힘들지만, 샤오미는 모방의 천재이기 때문에 목표를 정하고 모방을 대놓고 하자면 못할 분야도 아닐거라 생각은 듭니다.

-------------------

-------------------

Fitbit은 IPO가격이 20불이었고 상당 첫날 30불이 넘은 가격으로 첫 거래를 시작했습니다. 상당히 성공적으로 보였지면 사실 중국 샤오미가 치고나오기 전에 빨리 상장해야한다는 조급함도 보였습니다. IPO 타이밍은 정말 예술이었지요.

-------------------

Fitbit Earning 발표를 다시 뒤져봤습니다. 재무재표가 상당히 제가 맘에 들어하는 상태입니다. Gross Margin이 40%가 넘고 Operating Margin은 20%나 됩니다. 비싸게 팔린다는 얘기지요. 아직까진 샤오미 때문에 가격할인 압력도 크게 없다고 합니다. 캐쉬는 계속 늘고 있고 Debt은 없습니다.

어닝콜도 들어봤는데 상당히 고무적입니다. 우선 지난 분기가 상당히 좋았고, 앞으로도 좋게보고 있습니다. 지난 분기가 좋았던 점이 놀라운것은 섹터는 다르지만 애플 와치가 시장에서 할인공세를 벌일때였는데 핏빗이 큰 영향이 없었다는 것이고요. 상장후 첫번째 맞는 미국 쇼핑시즌에서 상당히 좋은 결과를 예상하고 있습니다. 그리고 새해가 시작하면 누구나 한번씩 하게되는 건강계획이나 살빼는 계획에 있어서 핏빗이 좋은 위치를 차지할것 같습니다.

내년초에 예정된 몇가지 새로운 디바이스가 아주 기다려진다고 전하고 있습니다. 어떤 형태의 device인지는 밝히지 않고 있습니다.

많이 가진 현금을 바탕을 M&A도 고려중이고 특정 분야의 회사를 얘기하진 않았습니다. M&A되는것도 고려중인지 묻고 싶었습니다.

CEO인 한국인 James이분은 어닝콜에서도 잘 리드하시는 것 같았습니다. 저는 한국인이라고 알고 들어서 한국인 억양이 많이 느껴졌지만 모르는 사람이 들었다면 그냥 약간의 아시안 엑센트가 있구나 할정도로 미국에서 오래동안 공부하시고 자라신것으로 보입니다.

이런저런 계산을 해보니 Fitbit의 지금 가격은 너무 싼것 같습니다. 12월 FRB미팅을 앞두고 상당히 변동성이 큰 마켓이지만 핏빗 주주가 되어야 겠습니다.

-------------------

For additional information regarding the non-GAAP financial measures, see “Non-GAAP Financial Measures” and “Reconciliation of GAAP to Non-GAAP Financial Measures” below.

Third Quarter 2015 Financial Highlights

Sold 4.8 million connected health and fitness devices

U.S. comprised 66% of Q3 revenue; APAC 16%, EMEA 12%, and Other Americas 6%

U.S. revenue grew 130% year-over-year; APAC 314%, EMEA 282%, and Other Americas 286%

Charge, Charge HR and Surge comprised 79% of revenue

Q3 Non-GAAP Gross Margin adjusted for international currency impact was 50.8%

OpEx comprised 28.6% of revenue in Q315, compared to 26.9% in Q215 and 25.0% in Q314

Q315 cash from operations increased 37x to $121.3 million compared to Q314

Cash, cash equivalents and marketable securities totaled $575.5 million at September 30, 2015, compared to $64.0 million atSeptember 30, 2014

Third Quarter 2015 and Recent Fitbit Operational Highlights

Continued strong market share and competitive position

Software updates to Surge, Charge and Charge HR leading into first full holiday season for those devices

Enhancements for other regions and cultures, such as integrating Baidu maps in China

Addition of Windows 10 integration; supported on more than 200 mobile and computing platforms

Marketing campaigns in 20 countries in second half 2015 vs. eight in 2014

Added over 20 new enterprise Corporate Wellness customers in the last four months

Expansion of global customer service capacity

Outlook and Guidance

Fitbit’s outlook for the fourth quarter of 2015 is as follows:

Revenue in the range of $620 to $650 million

Non-GAAP gross margin in the range of 48.0 to 49.0%

Adjusted EBITDA in the range of $80 to $100 million

Non-GAAP diluted net income per share in the range of $0.20 to $0.25

Non-GAAP diluted share count between 253 and 255 million

Stock-based compensation expense in the range of $18 to $20 million

Non-GAAP tax rate of approximately 33%

Fitbit’s outlook for the full year of 2015 is as follows:

Revenue in the range of $1.77 to $1.80 billion

Non-GAAP gross margin in the range of 48.0 to 48.5%

Adjusted EBITDA in the range of $345 to $365 million

Non-GAAP diluted net income per share in the range of $0.92 to $0.96

Non-GAAP diluted share count between 238 and 239 million

Stock-based compensation expense in the range of $44 to $46 million

Non-GAAP tax rate of approximately 33%

Lock-Up Release

Fitbit also announces today that Morgan Stanley & Co. LLC, on behalf of the underwriters of Fitbit’s initial public offering in June 2015, at the request of Fitbit, has agreed to release the lock-up restrictions for Fitbit’s employees and consultants as of October 31, 2015 with respect to approximately 2.3 million shares, which represents up to 10% of the shares of Fitbit common stock, options, and restricted stock units held by such employees and consultants. The release will be effective on November 4, 2015. This will allow Fitbit’s employees and consultants an opportunity in 2015 for liquidity prior to commencement of Fitbit’s quarter end blackout period, which would prohibit any sales until that period ends after the earnings release for the fourth quarter of 2015. The lock-up restrictions are scheduled to expire with respect to the remaining shares as originally planned on December 14, 2015.

추락하는데에는 정말 날개가 없네요. 다행히 chipset(QCT, QTI)은 놀랍게도 잘 팔리고 있다고 보여지네요. low end개수가 많아서 영업이익을 높히는데는 큰 도움은 안되고 있습니다만. 이마저도 화웨이랑 샤오미가 자기 AP로 넘어가게 되는 내년부터는 문제겠네요.

이번에는 라이센스(license, QTL)쪽이 더 문제가 있어보이네요. 중국정부랑 역사상 최고 벌금으로 다 끝났는것으로 보였으나 개별 업체랑 협상이 지지부진해서 돈이 입금이 안되고 있다고 합니다. 사인하자니 너무 싸고 중국 업체들은 바쁠것 없고 뭐 상황은 그런 상황인듯.

That would be the first full-year drop in this segment since fiscal 2009, when Nokia suspended royalty payments to Qualcomm over a patent dispute. That was eventually settled.

전분기대비 -44%나 영업이익(operating income)과 순이익(net income)이 감소한것은 정말 크네요. MSM shipment는 크게 차이가 없는것 보면 MSM 팔리는 부진이랑은 상관이 없어 보니고, 중국업체로부터 license fee를 상당히 못받고 있다고 봐야할듯.

-----------------

Qualcomm Profit Falls 44%

Struggles in patent licensing business overshadow positive signs in sales of smartphone chips

이런 Great Company가 지구상에 있다니 정말 같이 살고 있다는것만으로도 행복합니다. 살아 생전에 매분기별 실적과 매 신제품 발표회마다 사람을 설레이게 만드는 이런 회사를 또 만날수 있을까요? 만날수만 있다면 행운이지요, 그게 한국회사라면 더더욱.

-------------------

작년에 IPhone6가 나왔을때 마지막 두 분기만으로 100M개(37M + 63M) 1억대를 팔아해치웠지요. 앞으로 이런 기록을 크게 윗도는 것은 불가능할 것으로 예측되었는데, 이유는 하이엔드 폰 시장이 더이상 커지지 않고 경쟁은 더 치열해진다고 생각했기 때문이지요.

이번에 나온 결과로 IPhone6S 파괴력이 모든 경쟁자를 다 파괴할정도 엄청나다는 것이 들어났습니다. (같은 세그먼트에서 경쟁하는 모델은 다 작살났다고 봐야지요)

Iphone 판매량은 48M개로 으로 작년대비 28% 상승. 블랙프라이데이와 크리스마스가 껴있는 마지막 quarter에서는 작년동기대비 10%만 증가해도 70.4M. 그러면 118M(1억 1천 8백만)개를 년말 두분기에 판매하는 상황이 됩니다. 헐~ 대부분의 회사는 지금까지 판 모든 스마트폰을 다 더해도 1억개가 안되지요.

Gross Margin이 무려 40%. 순수한 SW도 아니고 물건만들어 팔아 장사하는데 40%가 말이안되지요.

Iphone개당 판매단가도 10%나 올라갔네요. 믿어지지가 않네요. 가격은 더 올랐는데 사람들은 더 못사서 난리나니.

The average selling price of an iPhone: $670 — up $67.

Apple included its holiday outlook in results for the fiscal fourth quarter, which ended on Sept. 26. For that period, the company posted net income of $11.1 billion, or $1.96 a share, while sales rose 22 percent to $51.5 billion. Analysts had predicted earnings of $1.88 a share on sales of $51 billion. The company had $205.7 billion in cash and investments on its balance sheet at the end of the quarter. Gross margin, a measure of profitability, widened to 39.9 percent.

Apple’s success largely hinges on the iPhone. The company sold 48 million handsets last quarter, up 22 percent from a year earlier and shy of analysts’ average prediction of 48.5 million shipments. The device generated sales of $32.2 billion, making it bigger than Microsoft Corp. and Facebook Inc.’s quarterly businesses combined. Introduced on Sept. 25, the newest models -- iPhone 6S and 6S Plus -- come with an improved camera, faster processor and new 3D Touch screens.

-------------------

안좋은 점은 IPAD판매량이 예상보다 낮았다는거. 이미 IPad는 실적과 상관성이 많이 떨어져서 큰 문제는 아닌것 같고요.

-------------------

애플 아이폰과 직접 경쟁하는 폰은 삼성 갤럭시 밖에 없는데, 판매량이 x작살 났다고 보여집니다.(프리미엄 폰 시장은 크게 늘지 않는데 아이폰이 다 쓸어버렸으니)

하지만 좋은 점은 이미 삼성에서 (이미 알고) 애플과 다이다이 경쟁이 아니라 따라하기 작전과 가격할인으로 몸을 낮쳤고, 주요 마케팅 포인트가 아이폰과 거의 비슷한데 좀더 싼(짝퉁보다는 좀더 고급스럽고)로 마케팅한 것이 주요했다고 보여집니다. 갤럭시 문닫을 뻔했는데 똘똘한 마케팅으로 그것은 살린것 같습니다. LG처럼 초프리미엄 어쩌구 투자한 한 새끼들은 다 짐싸서 나가게 해야하는데 LG는 그런것을 못해서 망해요. 초프리미엄 어쩌구 할때에 '아이폰과 똑같은데 반값' 이게 훨씬 장사꾼 답고 많은 사람의 잡을 구해줬을거라 생각됩니다. (물론 LG의 장사꾼이 아니라 기술자적 생각은 항상 존경하고 있습니다, 장사꾼인데 장사꾼 생각을 못하는 윗대가리들을 내보내야지)

-------------------

Apple Earning을 LIVE로 들어볼까하고 들어갔더니 상당히 까다롭네요. 다른 회사들처럼 그냥 browser하나로 들을수 있게해주는게 어려운게 아닌데. 이런것은 정말 짜증나지요. 제가 회사에서 주로 쓰는 기기는 WIn7과 리눅스인데. 쓸데없는 ITunes깔기고 뭐하고. 에라이~ 안듣는다.